A Guide to Fintech Security

A practical, founder-friendly guide to protecting fast-moving fintech products from the security threats that can stall growth, break trust, and trigger compliance headaches.

Introduction: Fintech Moves Fast, Risk Moves Faster

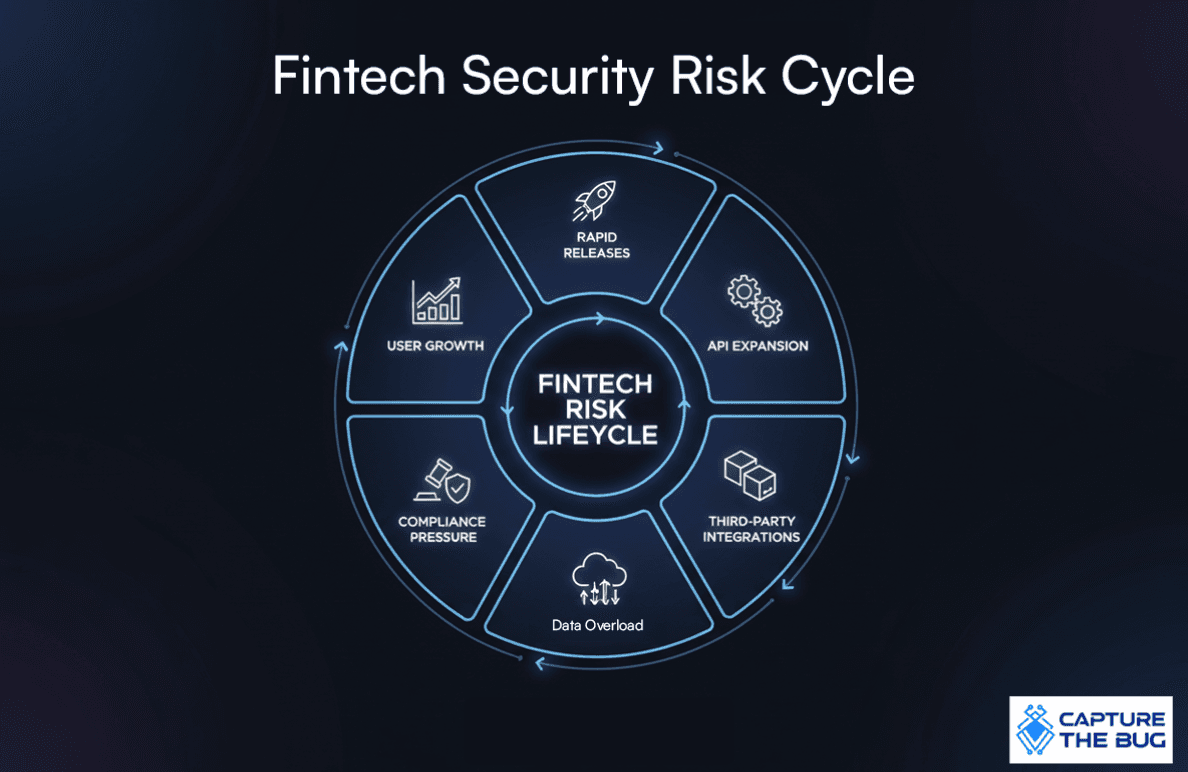

Fintech companies live in a world where trust is everything. Customers hand over significant personal and financial data every day, expecting platforms to keep it safe. Yet behind the scenes, fintech products are growing fast, adding new features, launching new APIs, and integrating third-party tools at a pace that introduces risks most teams never see coming.

This is why fintech security is no longer a box to check. It has become a business foundation. When a single misconfiguration can leak thousands of transaction records or a weak authentication flow can drain user accounts, security shifts from being a technical topic to a strategic one.

Capture The Bug works closely with fintech teams across New Zealand, Australia, and the United States, and the pattern is always the same. Fintech founders want speed, but they also want certainty. They want to innovate without worrying about what they cannot see.

This guide is written for them.

What Fintech Security Really Means Today

Fintech security covers the systems, controls, people, and processes required to keep customer data, financial transactions, and platform infrastructure safe from attacks. It protects three things that matter the most:

- Confidentiality: Customer financial data must remain private.

- Integrity: Transactions must remain accurate and tamper-free.

- Availability: Platforms must stay online even during incidents.

Fintechs face an unusually high threat level because they store data that criminals want. At the same time, they are expected to move faster than banks. That tension makes fintech security uniquely challenging and uniquely important.

The Real Risks Fintechs Face

Here are the risks security teams inside fintech platforms deal with every day.

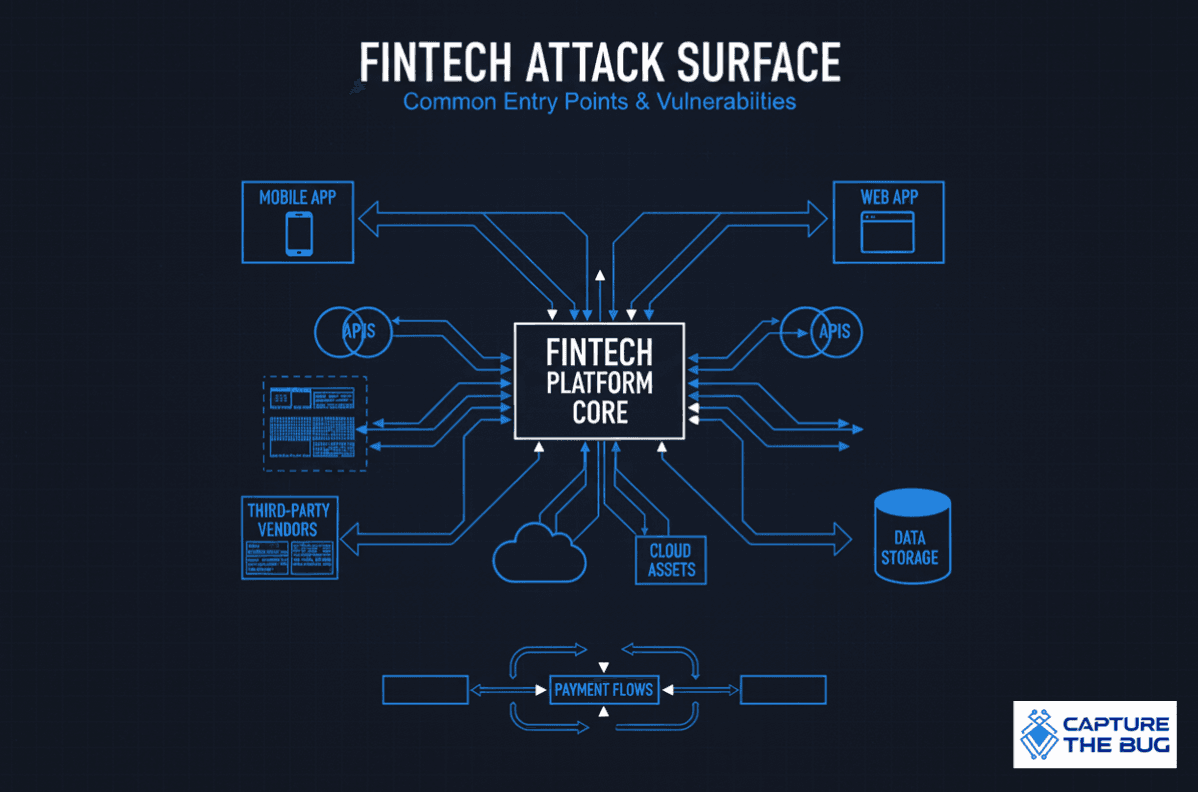

1. Weak API Security

Fintechs rely heavily on APIs for everything from onboarding to payment processing. APIs become the front door to the business. When validation is weak or logic is flawed, an attacker can exploit a single endpoint and escalate deeper.

Common API risks include:

- Unvalidated input

- Session hijacking

- Broken authentication

- Missing rate limits

This is one of the most common weaknesses discovered during pentests across fintech platforms.

2. Faulty Authentication and Access Controls

If authentication and authorization are not airtight, attackers gain the simplest path into financial data. Issues like easy-to-guess passwords, long-lasting sessions, and missing timeout controls allow attackers to impersonate users and perform unauthorized actions.

For fintech companies dealing with payments, lending, and digital wallets, this is the area where a single oversight can cause significant damage.

3. Third-Party and Vendor Exposure

Fintech platforms rarely operate in isolation. They depend on:

- KYC providers

- Payment processors

- Analytics tools

- Cloud services

Each integration expands the attack surface. A vulnerability inside a vendor can quickly become a vulnerability inside the fintech itself.

Without strict review processes, fintech leaders often discover these risks too late.

4. Data Storage and Transmission Gaps

Financial data moves constantly and must be protected at every step. Weak encryption, exposed logs, and insecure backups are common issues that lead to large-scale data leaks.

It is not always attackers who create the damage. Sometimes it is a small internal misconfiguration that goes unnoticed inside the engineering team for months.

Why Fintech Security Feels Hard

Security inside fintechs fails most often because of these challenges.

1. Regulatory Pressure

Fintechs must comply with standards like PCI DSS, ISO 27001, SOC 2, GDPR, and regional laws. Requirements evolve constantly and differ across markets. For founders, simply keeping track becomes a full-time job.

2. Innovation Outrunning Security

Fintechs compete in crowded markets. Features are released fast, integrations move quickly, and engineering teams sprint. If security is not integrated early, it becomes a fire drill right before an audit.

3. Legacy Infrastructure

Even modern fintechs integrate with old banking systems that were never designed for cloud-first platforms. These older systems introduce gaps that need ongoing validation.

4. Rapid Scaling

User growth is great until it exposes cracks in internal processes. As fintechs scale, they often lose visibility of their expanding attack surface. That is when unnoticed vulnerabilities grow in impact.

The Foundations of Strong Fintech Security

Here are the practices fintech companies use today to stay secure without slowing product delivery.

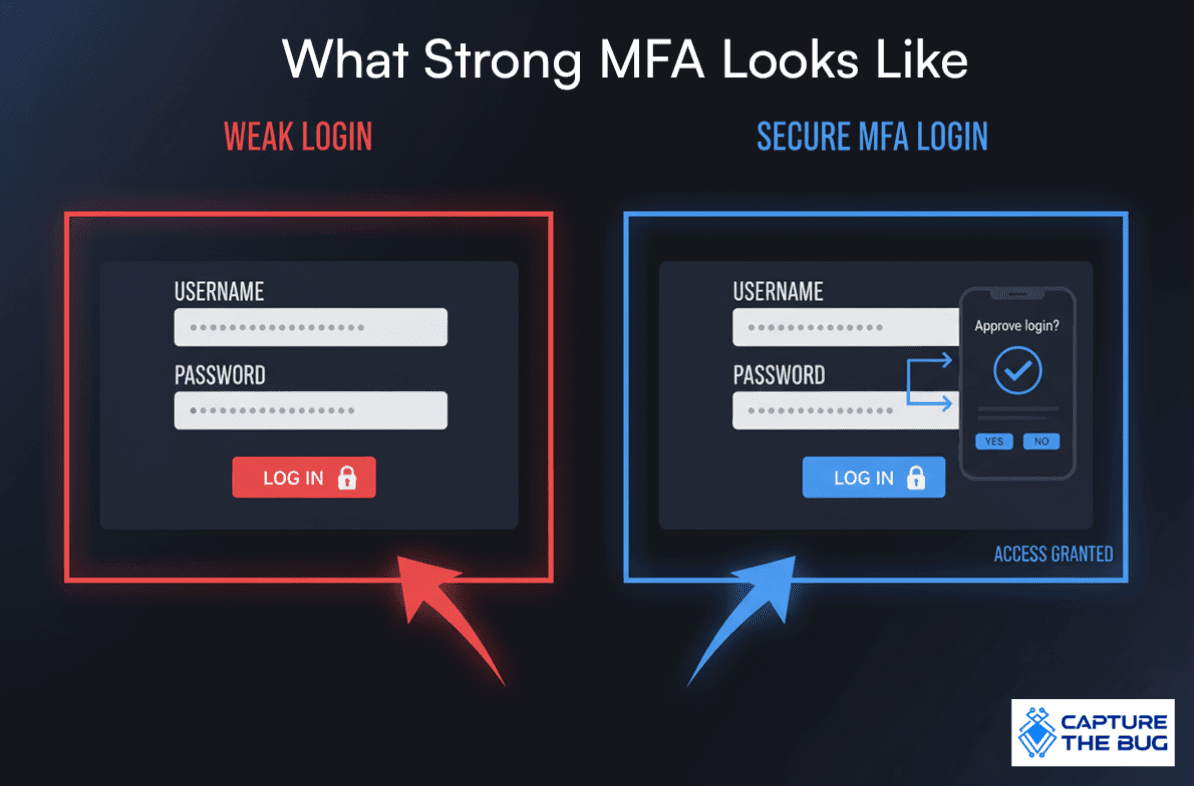

1. Strong Multi-Factor Authentication

Passwords alone cannot protect financial systems. Fintechs rely on MFA across all user and employee accounts. App-based or push notification–based authentication is preferred over SMS, which is vulnerable to SIM swapping.

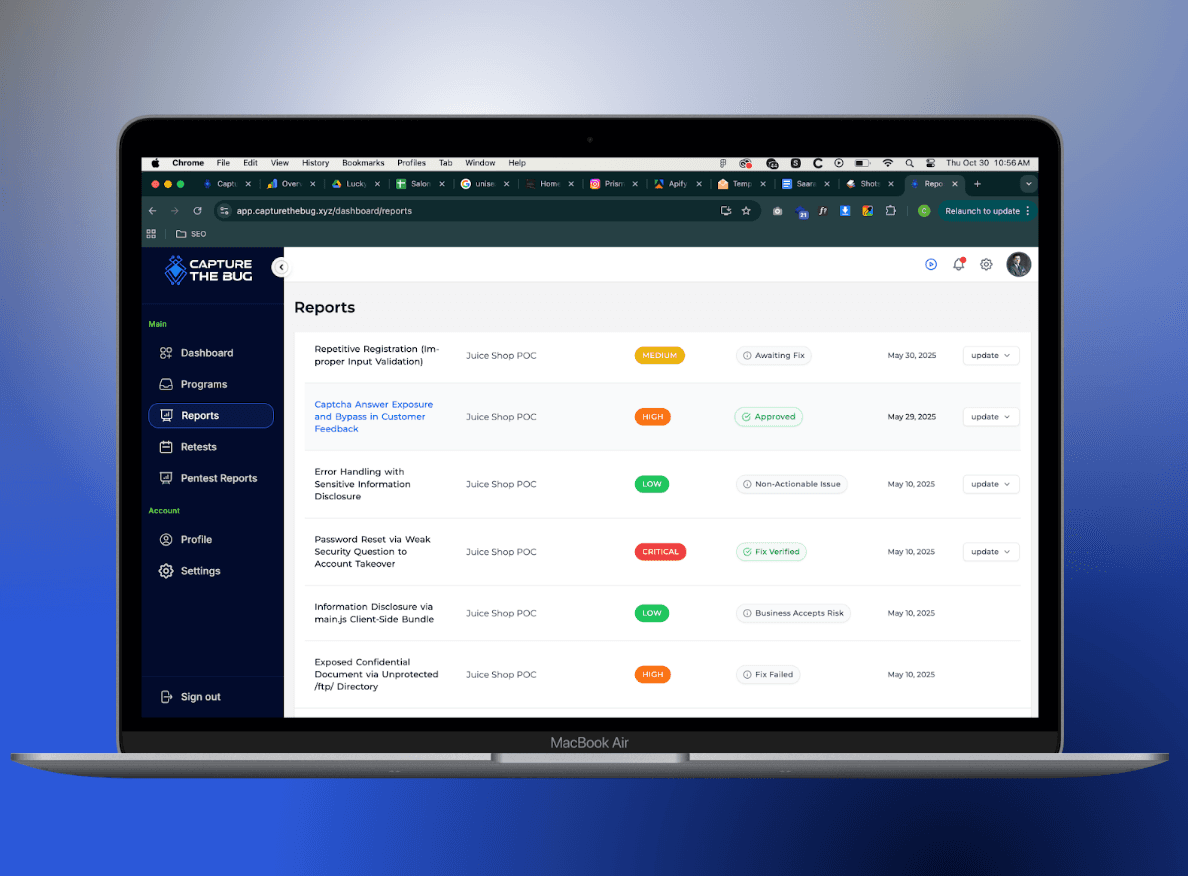

2. Regular Security Assessments and Pentesting

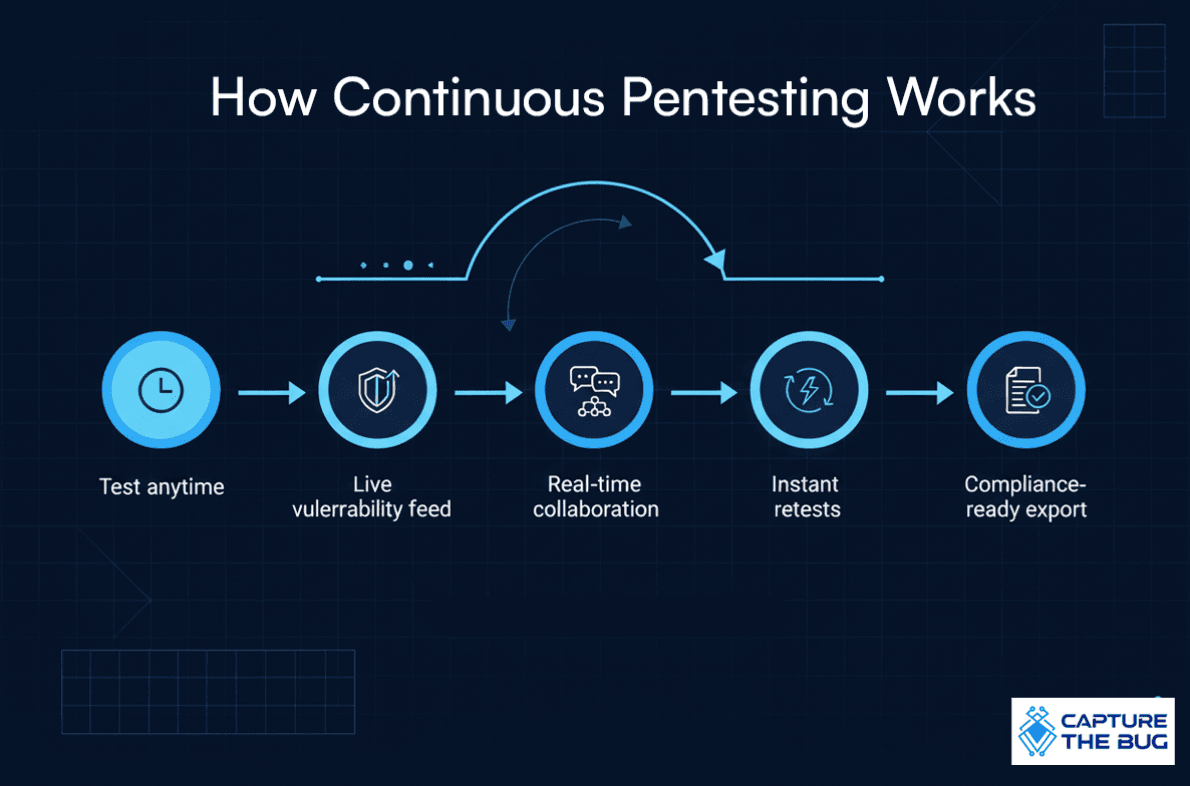

Security assessments uncover weaknesses before real attackers do. Fintech leaders are moving away from once-a-year pentests and toward continuous validation through modern PTaaS platforms. This ensures systems remain secure as the product evolves.

Platforms like Capture The Bug allow fintechs to:

- See vulnerabilities the moment they are found

- Collaborate directly with testers

- Track fixes in real time

- Export compliance-ready reports instantly

This supports the regulatory pressures fintechs face while keeping teams agile.

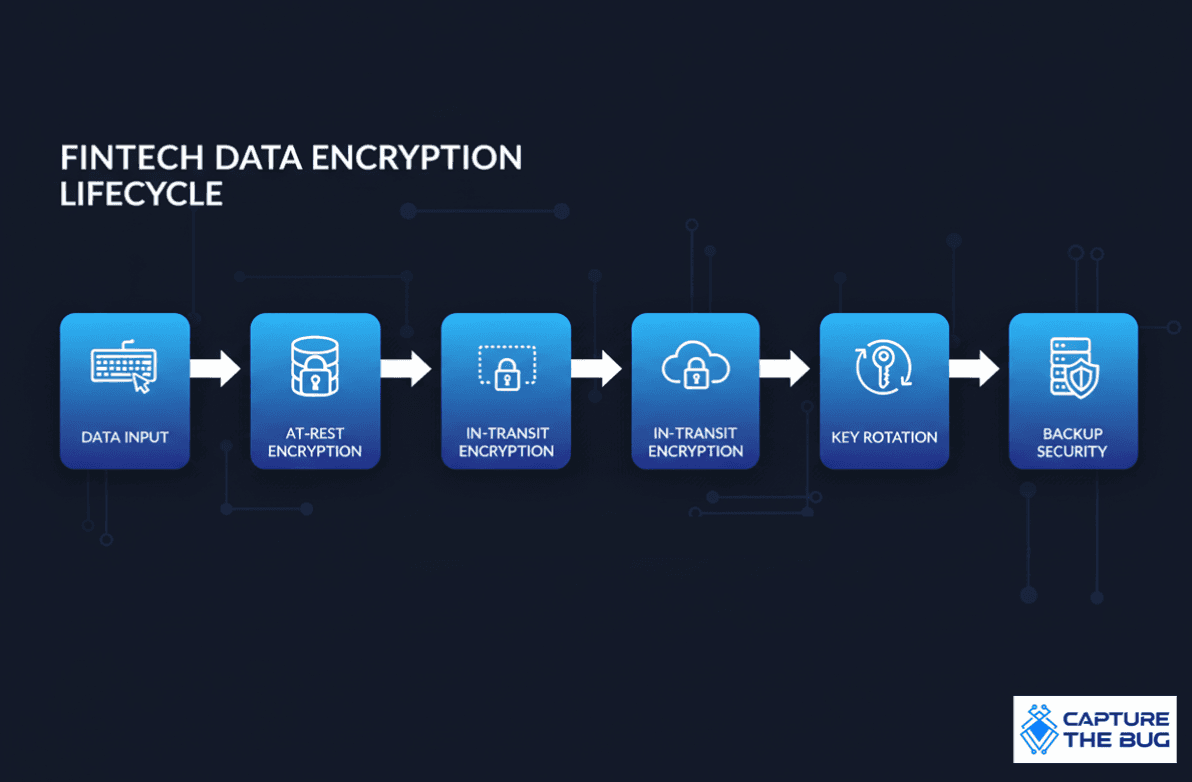

3. Encryption Everywhere

Fintech platforms use strong encryption protocols for:

- Data in transit

- Data at rest

- Backups

- Payment information

Key rotation policies, separation of duties, and secure key storage are critical components of a strong data protection program.

4. Incident Response Plans

Breaches can happen even in well-secured systems. Fintechs need clearly documented incident response processes that define roles, communication plans, and technical steps.

Teams that practice incident response recover quickly. Teams that do not often lose valuable time during an attack.

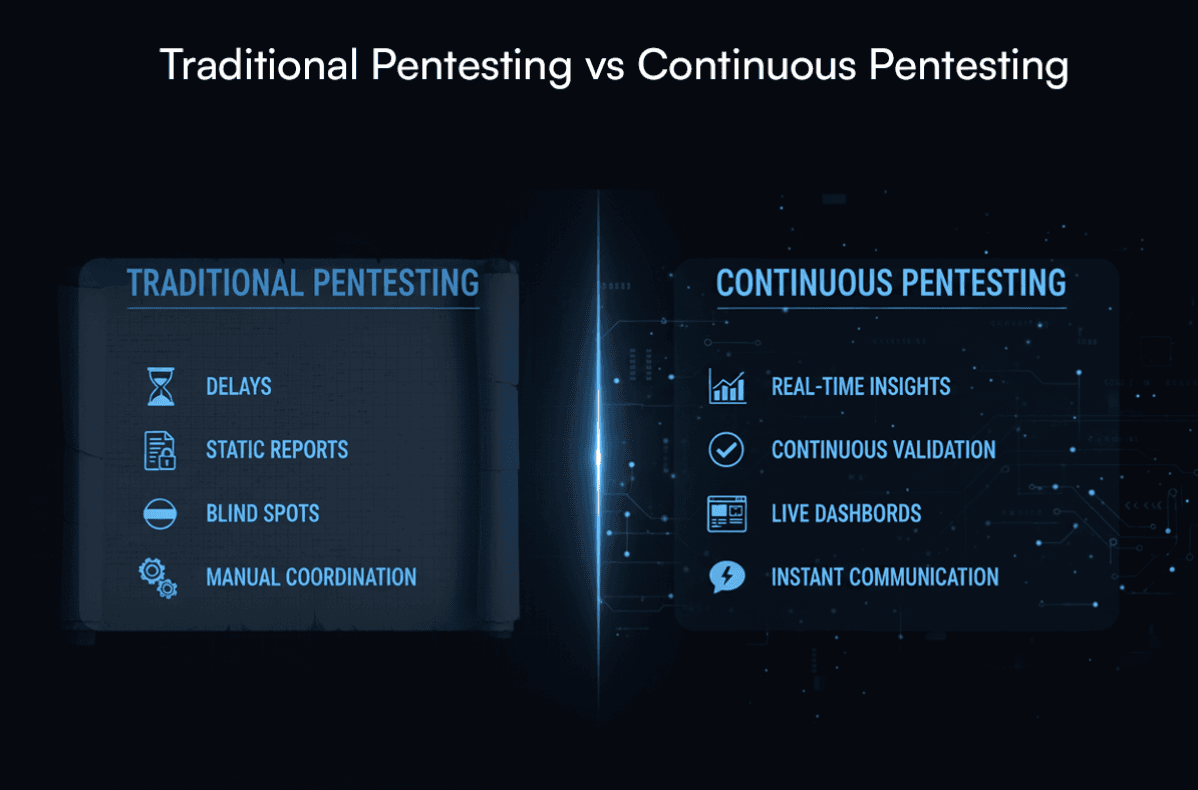

How Fintechs Use PTaaS to Stay Ahead

Traditional pentesting gives a one-time report. Fintechs have learned that the real risk lies in the time between tests. A vulnerability introduced today cannot wait months for discovery.

This is why fast-growing fintechs are shifting to continuous pentesting delivered through PTaaS platforms like Capture The Bug. The platform provides:

- On-demand testing

- Real-time results

- Direct collaboration with testers

- Instant retests

- Audit-ready documentation

This model closes the blind spots caused by scheduled audits. It gives fintech leaders real visibility and reduces risk dramatically.

What Fintech Leaders Should Focus on in 2025

Based on industry patterns across New Zealand, Australia, and the USA, here is where fintechs are investing their security focus.

- 1. API Hardening

- 2. Identity Security

- 3. Payment Flows

- 4. Compliance Readiness

- 5. Continuous Testing

Final Thoughts

Fintech security is not just a technical problem. It is a business strategy. When trust is the currency, security becomes the foundation that allows companies to grow, scale, and enter new markets confidently.

The most successful fintechs today combine disciplined security practices with continuous testing. They do not rely on scheduled checks. They adopt real-time visibility and collaboration so teams can fix issues as they appear, not after they cause harm.

Capture The Bug supports this shift by providing fintech teams with continuous pentesting, real-time dashboards, CREST-certified testers, and compliance-ready outputs. It is a simpler, clearer, and faster way to keep financial technology secure every day.

Ready to Secure Your Fintech?

See how Capture The Bug's CREST-certified PTaaS platform delivers continuous testing, real-time collaboration, and compliance-ready outputs tailored for fintech teams.

FAQ

1. What is fintech security?

It refers to the controls, processes, and protections that keep financial data and digital transactions safe from cyber threats.

2. Why do fintech platforms face higher risk?

They store valuable financial information, operate fast, and integrate with multiple third-party systems.

3. What is the role of pentesting in fintech?

Pentesting helps identify weaknesses before attackers find them and supports compliance requirements.

4. How does continuous pentesting help fintech teams?

It provides real-time visibility, faster remediation, and always-on assurance as new features and updates are released.

5. What should fintechs prioritize in 2025?

Strengthening APIs, improving identity security, protecting payment flows, and adopting continuous testing models.